The Special Tax Regime applicable to workers, professionals, entrepreneurs, and investors moving to Spanish territory (in Spanish, Régimen fiscal especial aplicable a los trabajadores, profesionales, emprendedores e inversores desplazados a territorio español), provided for in Article 93 of Law 35/2006, of November 28, on the Personal Income Tax in Spain, commonly known as the Beckham Law, establishes that certain requirements must be met to benefit from the tax advantage. That is, it is not applicable to any taxpayer who wishes to apply it. The preliminary requirement is to obtain the status of a tax resident in Spain, but apart from that, there are other requirements related to employment, deadlines, documentation, etc.

Once it is verified that all the requirements are met, it will be necessary to formally submit the corresponding application for the Beckham Law to the Spanish Tax Agency. Additionally, a series of documents must be attached to this application to prove compliance with the requirements.

It is important to note that the requirements set forth in the legislation may seem clear and precise at first glance, but the reality is that they are often open to interpretation. Therefore, it is crucial to be very careful when analyzing the case and preparing the documentation because any error, no matter how minor it may seem, can lead to the loss or denial of the Beckham Law.

The following briefly describes each of the requirements that must be met to apply for the Beckham Law:

The regulations establish that the applicant cannot have been a tax resident in Spain at any time during the five years prior to their move to Spain.

In this regard, it is important to understand that tax residence is defined according to specific criteria that include the duration of the stay in the country, the location of the main center of economic interests, or the usual residence of the spouse and/or dependent children.

The essential question is, what determines whether someone can be considered a tax resident in Spain? The answer is that there are three ways to be considered a tax resident in Spain:

It should be noted that a person can be considered a tax resident in Spain if any of the three aforementioned situations are met (it is sufficient if one of them is met). That said, the 183-day rule is usually the most used.

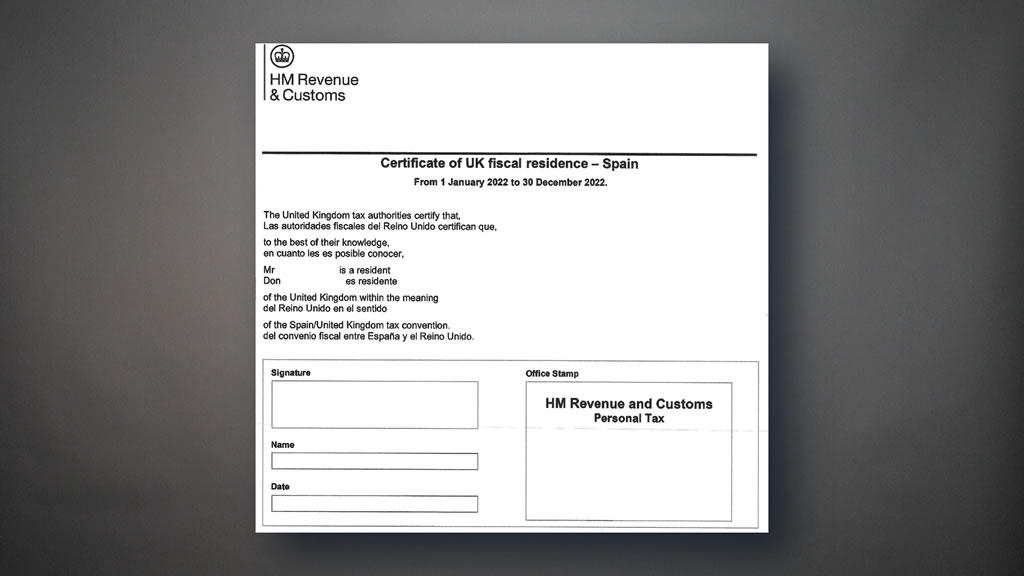

To verify compliance with this requirement, the Spanish tax authorities may request documentation or evidence proving that the applicant has not been a tax resident in Spain for the last five years. This may include tax returns and tax residence certificates from other countries, among other documents.

Another essential aspect to analyze is whether a person is or will be considered a tax resident upon their arrival in Spain. This is crucial because the Beckham Law is an optional regime available only to those who move to Spain and become tax residents in the country. Thus, it only makes sense to consider the Beckham Law if this tax resident status is met, not so much because it is specifically established in the norm, but because the Beckham Law aims to offer a tax resident a treatment similar to that of a non-tax resident. If one is not a tax resident in Spain, then the Beckham Law would not provide any advantage.

Regarding tax residency, it is important to highlight that the Beckham Law is only applicable if tax residency is acquired through the first mentioned path, i.e., the one that involves staying more than 183 days in Spanish territory. The reason for this requirement is that the Beckham Law is intended for those who actually move to Spain. Therefore, the legislator included this requirement to try to prevent the abusive use of the Beckham Law. Although it is very rare, this could lead to absurd situations. For example, an individual who spends less than 183 days in Spanish territory during the calendar year but becomes a Spanish tax resident by any of the other means mentioned (economic interests center or vital interests center route) would not be entitled to apply for the Beckham Law.

The previous sections defined the Spanish internal rules for determining if someone can be considered a tax resident in Spain. However, it could happen that, according to the internal rules of another country, that person could also be considered a tax resident in that other country. In these cases, Double Taxation Agreements (DTAs) come into play, which are international treaties between two countries where, among other things, “tie-breaker rules” are established. These rules serve to define in which of the two countries a person is considered a tax resident. These “tie-breaker rules” only come into play when a person is considered a tax resident in both countries according to the internal rules of each.

One of the requirements of the Beckham Law is that the move to Spain be for work-related reasons. This requirement might seem quite straightforward at first glance, but it often proves to be the most problematic of all. There are, essentially, two elements that must be considered:

The concept of “work” in the context of the Beckham Law is specifically defined in the legislation, which establishes up to 7 situations in which it will be understood that the individual has begun working in Spain:

The relocation to Spanish territory must occur as a result of the work to be carried out in Spain. However, the regulations do not specify in which cases there is considered to be a causal link between the move to Spain and the start of work, so it is open to interpretation.

A long period between the move to Spain and the start of work can be an indicator, among other factors, that such a causal relationship does not exist. Nevertheless, there are different types of evidence that can demonstrate causality. For example, the binding consultation V1163/2017 of the Dirección General de Tributos (an agency dependent on the Ministry of Finance whose binding consultations must be respected by the Spanish Tax Agency) indicates that if the move to Spain occurred due to the acceptance of a job offer from a Spanish company, and it can be shown that the job offer was received before moving to Spain, this would be clear evidence of the existence of such a causal link. Even without a job offer, if work begins a few weeks after moving to Spain, the chances of convincing the tax authorities are considerably high.

This requirement sometimes proves problematic because reality is often more complex than the regulations suggest. Therefore, it is worthwhile to plan the move in such a way that the causal relationship is as clear as possible.

Firstly, it is necessary to mention that the concept of “permanent establishment” is provided for in the regulations for those who have a business in Spain, even if they do not reside in Spain. In this case, those subject to the Beckham Law must reside in Spain, so sometimes confusing situations arise.

In any case, this requirement basically means that one cannot carry out an activity as a freelancer (“autónomo”) in Spain, outside of the specifically provided cases (conducting an entrepreneurial activity; providing services to start-ups; or conducting training, research, development, and innovation activities).

Special care must be taken with tax-transparent or “pass-through entities,” such as the “Limited Liability Company (LLC)” from the United States, the “Limited Liability Partnership (LLP)” from the United Kingdom, or the “Kommanditgesellschaft (KG)” from Germany. The reason is that the incomes derived from such tax-transparent entities are directly attributed to their partners. The problem is that, depending on the circumstances, the Spanish Tax Agency might consider that such incomes have been obtained through a permanent establishment located in Spanish territory, which would be incompatible with the Beckham Law.

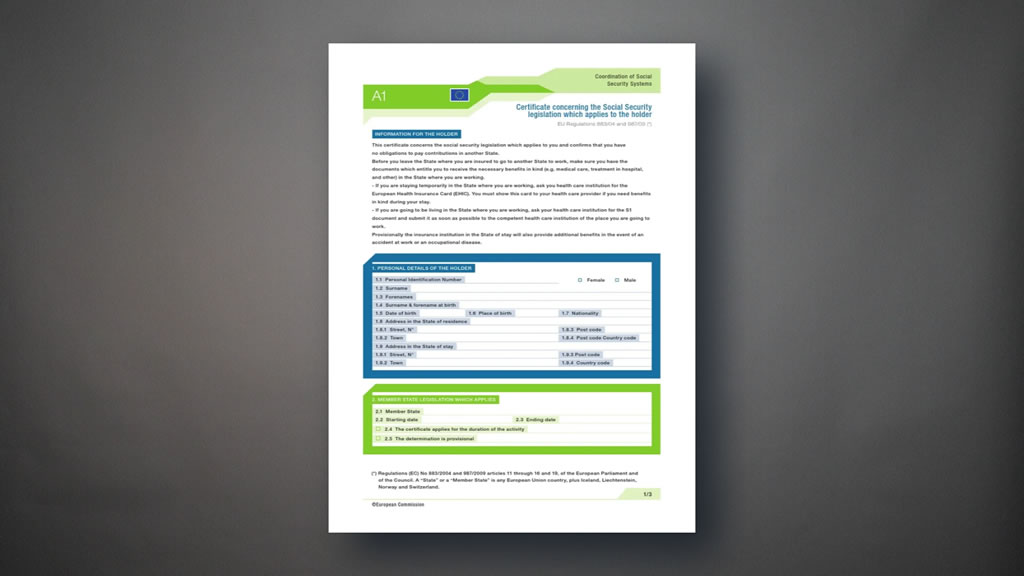

It is absolutely essential to submit the application on time because otherwise, the application will automatically be rejected. In this sense, the maximum period is six months from the start of the activity. This start is determined by the date of registration with the Social Security in Spain or by the documentation that allows for the maintenance of Social Security in the country of origin. If registration with Social Security is not mandatory, the document that justifies the start of the activity will be taken as a reference.

On the other hand, it is very important to provide, along with the Beckham Law application, all the necessary documentation, and moreover to do so without errors. Normally, if all the documentation is not provided correctly, the Tax Agency will give another opportunity to do so correctly. However, when this occurs, the Tax Agency tends to take the opportunity to request any other documentation they deem appropriate, which would decrease the chances of obtaining a favorable result in the application process. For example, the Tax Agency might request the submission of an additional document (for which they usually grant a period of 10 business days), the acquisition of which, for whatever reason, might not be possible within the deadline (it could be, for example, a document issued by a public administration in another country, the issuance of which requires months).

There is the possibility that certain direct family members can also benefit from the Beckham Law, without needing to meet the strict requirements regarding work and relocation.

Specifically, the regulations establish that the direct family members of a taxpayer can also apply, if they wish, for the Beckham Law. The following are considered direct family members of the taxpayer (whose application must already have been approved):

Notwithstanding the above, these family members must also meet some requirements:

This special regime will apply during successive tax periods provided that the aforementioned requirements are met and the Beckham Law continues to apply to the main taxpayer.

It is also mentioned that these family members can move to Spain before or after the main taxpayer’s move, but they must ensure not to acquire tax residency in Spain before the first tax period in which the special regime applies to the main taxpayer, or if the move is later, that this last tax period has not ended.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}